Point estimator

A statistical estimator whose values are points in the set of values of the quantity to be estimated.

Suppose that in the realization  of the random vector

of the random vector  , taking values in a sample space

, taking values in a sample space  ,

,  , the unknown parameter

, the unknown parameter  (or some function

(or some function  ) is to be estimated. Then any statistic

) is to be estimated. Then any statistic  producing a mapping of the set

producing a mapping of the set  into

into  (or into the set of values of

(or into the set of values of  ) is called a point estimator of

) is called a point estimator of  (or of the function

(or of the function  to be estimated). Important characteristics of a point estimator

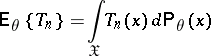

to be estimated). Important characteristics of a point estimator  are its mathematical expectation

are its mathematical expectation

|

and the covariance matrix

|

The vector  is called the error vector of the point estimator

is called the error vector of the point estimator  . If

. If

|

is the zero vector for all  , then one says that

, then one says that  is an unbiased estimator of

is an unbiased estimator of  or that

or that  is free of systematic errors; otherwise,

is free of systematic errors; otherwise,  is said to be biased, and the vector

is said to be biased, and the vector  is called the bias or systematic error of the point estimator. The quality of a point estimator can be defined by means of the risk function (cf. Risk of a statistical procedure).

is called the bias or systematic error of the point estimator. The quality of a point estimator can be defined by means of the risk function (cf. Risk of a statistical procedure).

References

| [1] | H. Cramér, "Mathematical methods of statistics" , Princeton Univ. Press (1946) |

| [2] | I.A. Ibragimov, R.Z. [R.Z. Khas'minskii] Has'minskii, "Statistical estimation: asymptotic theory" , Springer (1981) (Translated from Russian) |

Comments

References

| [a1] | E.L. Lehmann, "Theory of point estimation" , Wiley (1983) |

Point estimator. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Point_estimator&oldid=16171