Stochastic differential

A random interval function  defined by the formula

defined by the formula

|

for every process  in the class of semi-martingales

in the class of semi-martingales  , with respect to a stochastic basis

, with respect to a stochastic basis  . In the family of stochastic differentials

. In the family of stochastic differentials  one introduces addition

one introduces addition  , multiplication by a process

, multiplication by a process  and the product operation

and the product operation  according to the following formulas:

according to the following formulas:

;

;

(a stochastic integral,

(a stochastic integral,  being a locally bounded predictable process which is adapted to the filtration

being a locally bounded predictable process which is adapted to the filtration  );

);

, where

, where  and

and  are the left-continuous versions of

are the left-continuous versions of  and

and  .

.

It then turns out that

|

where  is an arbitrary decomposition of the interval

is an arbitrary decomposition of the interval  , l.i.p. is the limit in probability, and

, l.i.p. is the limit in probability, and  .

.

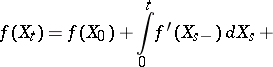

In stochastic analysis, the principle of "differentiation" of random functions, or Itô formula, is of importance: If  and the function

and the function  , then

, then

|

and

| (1) |

where  is the partial derivative with respect to the

is the partial derivative with respect to the  -th coordinate. In particular, it can be inferred from (1) that if

-th coordinate. In particular, it can be inferred from (1) that if  , then

, then

| (2) |

|

where  is the continuous martingale part of

is the continuous martingale part of  ,

,  .

.

Formula (2) can be given the following form:

|

|

where  is the quadratic variation of

is the quadratic variation of  .

.

References

| [1] | K. Itô, S. Watanabe, "Introduction to stochastic differential equations" K. Itô (ed.) , Proc. Int. Symp. Stochastic Differential Equations Kyoto, 1976 , Wiley (1978) pp. I-XXX |

| [2] | I.I. Gikhman, A.V. Skorokhod, "Stochastic differential equations and their applications" , Kiev (1982) (In Russian) |

Comments

The product  is more often written as

is more often written as  , where the so-called "square bracket"

, where the so-called "square bracket"  is the process with finite variation such that

is the process with finite variation such that  . When

. When  , one obtains the quadratic variation

, one obtains the quadratic variation  used at the end of the main article. Actually, it is a probabilistic quadratic variation: when

used at the end of the main article. Actually, it is a probabilistic quadratic variation: when  is a standard Brownian motion,

is a standard Brownian motion,  is the Lebesgue measure, but the true quadratic variation of the paths is almost surely infinite. See also Semi-martingale; Stochastic integral; Stochastic differential equation.

is the Lebesgue measure, but the true quadratic variation of the paths is almost surely infinite. See also Semi-martingale; Stochastic integral; Stochastic differential equation.

For the study of continuous-path processes evolving on non-flat manifolds the Itô stochastic differential is inconvenient, because the Itô formula (2) is incompatible with the ordinary rules of calculus relating different coordinate systems. A coordinate-free description can be obtained using the Stratonovich differential; see [a1], [a2], Chapt. 5, [a3], and Stratonovich integral.

References

| [a1] | K.D. Elworthy, "Stochastic differential equations on manifolds" , Cambridge Univ. Press (1982) |

| [a2] | N. Ikeda, S. Watanabe, "Stochastic differential equations and diffusion processes" , North-Holland (1989) pp. 97ff |

| [a3] | P.A. Meyer, "Geometrie stochastiques sans larmes" J. Azéma (ed.) M. Yor (ed.) , Sem. Probab. Strassbourg XV , Lect. notes in math. , 850 , Springer (1981) pp. 44–102 |

| [a4] | I. Karatzas, S.E. Shreve, "Brownian motion and stochastic calculus" , Springer (1988) |

| [a5] | L.C.G. Rogers, D. Williams, "Diffusion, Markov processes, and martingales" , 2. Itô calculus , Wiley (1987) |

| [a6] | S. Albeverio, J.E. Fenstad, R. Høegh-Krohn, T. Lindstrøm, "Nonstandard methods in stochastic analysis and mathematical physics" , Acad. Press (1986) |

Stochastic differential. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Stochastic_differential&oldid=48846