Lévy metric

A metric  in the space

in the space  of distribution functions (cf. Distribution function) of one-dimensional random variables such that:

of distribution functions (cf. Distribution function) of one-dimensional random variables such that:

|

|

for any  . It was introduced by P. Lévy (see [1]). If between the graphs of

. It was introduced by P. Lévy (see [1]). If between the graphs of  and

and  one inscribes squares with sides parallel to the coordinate axes (at points of discontinuity of a graph vertical segments are added), then a side of the largest of them is equal to

one inscribes squares with sides parallel to the coordinate axes (at points of discontinuity of a graph vertical segments are added), then a side of the largest of them is equal to  .

.

The Lévy metric can be regarded as a special case of the Lévy–Prokhorov metric. The definition of the Lévy metric carries over to the set  of all non-decreasing functions on

of all non-decreasing functions on  (infinite values of the metric being allowed).

(infinite values of the metric being allowed).

Most important properties of the Lévy metric.

1) The Lévy metric induces a weak topology in  (cf. Distributions, convergence of). The metric space (

(cf. Distributions, convergence of). The metric space ( ) is separable and complete. Convergence of a sequence of functions from

) is separable and complete. Convergence of a sequence of functions from  in the metric

in the metric  is equivalent to complete convergence.

is equivalent to complete convergence.

2) If  and if

and if

|

then for any  ,

,

|

3) Regularity of the Lévy metric: For any  ,

,

|

(here  denotes convolution, cf. Convolution of functions). A consequence of this property is the property of semi-additivity:

denotes convolution, cf. Convolution of functions). A consequence of this property is the property of semi-additivity:

|

and the "smoothing inequality" :

|

( being a distribution that is degenerate at zero).

being a distribution that is degenerate at zero).

4) If  ,

,  , then

, then

|

5) If  ,

,  , is an absolute moment of the distribution

, is an absolute moment of the distribution  , then

, then

|

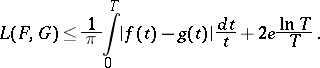

6) The Lévy metric on  is related to the integral mean metric

is related to the integral mean metric

|

by the inequality

|

7) The Lévy metric on  is related to the uniform metric

is related to the uniform metric

|

by the relations

| (*) |

where

|

( is the concentration function for

is the concentration function for  ). In particular, if one of the functions, for example

). In particular, if one of the functions, for example  , has a uniformly bounded derivative, then

, has a uniformly bounded derivative, then

|

A consequence of (*) is the Pólya–Glivenko theorem on the equivalence of weak and uniform convergence in the case when the limit distribution is continuous.

8) If  , where

, where  and

and  are constants, then for any

are constants, then for any  ,

,

|

(in particular, the Lévy metric is invariant with respect to a shift of the distributions) and

|

9) If  and

and  are the characteristic functions (cf. Characteristic function) corresponding to the distributions

are the characteristic functions (cf. Characteristic function) corresponding to the distributions  and

and  , then for any

, then for any  ,

,

|

The concept of the Lévy metric can be extended to the case of distributions in  .

.

References

| [1] | P. Lévy, "Théorie de l'addition des variables aléatoires" , Gauthier-Villars (1937) |

| [2] | V.M. Zolotarev, "Estimates of the difference between distributions in the Lévy metric" Proc. Steklov Inst. Math. , 112 (1973) pp. 232–240 Trudy Mat. Inst. Steklov. , 112 (1971) pp. 224–231 |

| [3] | V.M. Zolotarev, V.V. Senatov, "Two-sided estimates of Lévy's metric" Theor. Probab. Appl. , 20 (1975) pp. 234–245 Teor. Veroyatnost. i Primenen. , 20 : 2 (1975) pp. 239–250 |

| [4] | Yu.V. Linnik, I.V. Ostrovskii, "Decomposition of random variables and vectors" , Amer. Math. Soc. (1977) (Translated from Russian) |

Comments

A word of warning. In the Soviet mathematical literature (and in the main article above), distribution functions are usually left continuous, whereas in the West they are right continuous. So slight changes must be made in 2) or 7).

Let  be a distribution function or, more generally, a non-decreasing left-continuous function. Then

be a distribution function or, more generally, a non-decreasing left-continuous function. Then  has a countable set of discontinuity points. The complement of this set is called the continuity set

has a countable set of discontinuity points. The complement of this set is called the continuity set  of

of  . A series of distribution functions

. A series of distribution functions  is said to converge weakly to a distribution

is said to converge weakly to a distribution  if this is the case on the continuity set

if this is the case on the continuity set  of

of  . The series converges completely if moreover

. The series converges completely if moreover  and

and  . Cf. also Convergence of distributions and Convergence, types of.

. Cf. also Convergence of distributions and Convergence, types of.

References

| [a1] | P. Billingsley, "Convergence of probability measures" , Wiley (1968) |

| [a2] | W. Hengartner, R. Theodorescu, "Concentration functions" , Acad. Press (1973) |

| [a3] | M. Loève, "Probability theory" , v. Nostrand (1963) pp. 178 |

Lévy metric. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=L%C3%A9vy_metric&oldid=14153