A posteriori distribution

A conditional probability distribution of a random variable, to be contrasted with its unconditional or a priori distribution.

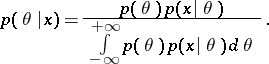

Let  be a random parameter with an a priori density

be a random parameter with an a priori density  , let

, let  be a random result of observations and let

be a random result of observations and let  be the conditional density of

be the conditional density of  when

when  ; then the a posteriori distribution of

; then the a posteriori distribution of  for a given

for a given  , according to the Bayes formula, has the density

, according to the Bayes formula, has the density

|

If  is a sufficient statistic for the family of distributions with densities

is a sufficient statistic for the family of distributions with densities  , then the a posteriori distribution depends not on

, then the a posteriori distribution depends not on  itself, but on

itself, but on  . The asymptotic behaviour of the a posteriori distribution

. The asymptotic behaviour of the a posteriori distribution  as

as  , where

, where  are the results of independent observations with density

are the results of independent observations with density  , is "almost independent" of the a priori distribution of

, is "almost independent" of the a priori distribution of  .

.

For the role played by a posteriori distributions in the theory of statistical decisions, see Bayesian approach.

References

| [1] | S.N. Bernshtein, "Probability theory" , Moscow-Leningrad (1946) (In Russian) |

Comments

References

| [a1] | E. Sverdrup, "Laws and chance variations" , 1 , North-Holland (1967) pp. 214ff |

A posteriori distribution. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=A_posteriori_distribution&oldid=11777