Regression matrix

The matrix  of regression coefficients (cf. Regression coefficient)

of regression coefficients (cf. Regression coefficient)  ,

,  ,

,  , in a multi-dimensional linear regression model,

, in a multi-dimensional linear regression model,

| (*) |

Here  is a matrix with elements

is a matrix with elements  ,

,  ,

,  , where

, where  ,

,  , are observations of the

, are observations of the  -th component of the original

-th component of the original  -dimensional random variable,

-dimensional random variable,  is a matrix of known regression variables

is a matrix of known regression variables  ,

,  ,

,  , and

, and  is the matrix of errors

is the matrix of errors  ,

,  ,

,  , with

, with  . The elements

. The elements  of the regression matrix

of the regression matrix  are unknown and have to be estimated. The model (*) is a generalization to the

are unknown and have to be estimated. The model (*) is a generalization to the  -dimensional case of the general linear model of regression analysis.

-dimensional case of the general linear model of regression analysis.

References

| [1] | M.G. Kendall, A. Stuart, "The advanced theory of statistics" , 3. Design and analysis, and time series , Griffin (1983) |

Comments

In econometrics, for example, a frequently used model is that one has  variables

variables  to be explained (endogenous variables) in terms of

to be explained (endogenous variables) in terms of  explanatory variables

explanatory variables  (exogenous variables) by means of a linear relationship

(exogenous variables) by means of a linear relationship  . Given

. Given  sets of measurements (with errors),

sets of measurements (with errors),  , the matrix of relation coefficients

, the matrix of relation coefficients  is to be estimated. The model is therefore

is to be estimated. The model is therefore

|

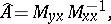

With the assumption that the  have zero mean and are independently and identically distributed with normal distribution, that is, the so-called standard linear multiple regression model or, briefly, linear model or standard linear model. The least squares method yields the optimal estimator:

have zero mean and are independently and identically distributed with normal distribution, that is, the so-called standard linear multiple regression model or, briefly, linear model or standard linear model. The least squares method yields the optimal estimator:

|

where  ,

,  . In the case of a single endogenous variable,

. In the case of a single endogenous variable,  , this can be conveniently written as

, this can be conveniently written as

|

where  is the column vector of observations

is the column vector of observations  and

and  is the

is the  observation matrix consisting of the rows

observation matrix consisting of the rows  ,

,  . Numerous variants and generalizations are considered [a1], [a2]; cf. also Regression analysis.

. Numerous variants and generalizations are considered [a1], [a2]; cf. also Regression analysis.

References

| [a1] | E. Malinvaud, "Statistical methods of econometrics" , North-Holland (1970) (Translated from French) |

| [a2] | H. Theil, "Principles of econometrics" , North-Holland (1971) |

Regression matrix. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Regression_matrix&oldid=48475