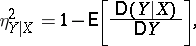

Correlation ratio

A characteristic of dependence between random variables. The correlation ratio of a random variable  relative to a random variable

relative to a random variable  is the expression

is the expression

|

where  is the variance of

is the variance of  ,

,  is the conditional variance of

is the conditional variance of  given

given  , which characterizes the spread of

, which characterizes the spread of  about its conditional mathematical expectation

about its conditional mathematical expectation  for a given value of

for a given value of  . Invariably,

. Invariably,  . The equality

. The equality  corresponds to non-correlated random variables;

corresponds to non-correlated random variables;  if and only if there is an exact functional relationship between

if and only if there is an exact functional relationship between  and

and  ; if

; if  is linearly dependent on

is linearly dependent on  , the correlation ratio coincides with the squared correlation coefficient. The correlation ratio is non-symmetric in

, the correlation ratio coincides with the squared correlation coefficient. The correlation ratio is non-symmetric in  and

and  , and so, together with

, and so, together with  , one considers

, one considers  (the correlation ratio of

(the correlation ratio of  relative to

relative to  , defined analogously). There is no simple relationship between

, defined analogously). There is no simple relationship between  and

and  . See also Correlation (in statistics).

. See also Correlation (in statistics).

Correlation ratio. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Correlation_ratio&oldid=46528