Canonical correlation coefficients

Maximum values of correlation coefficients between pairs of linear functions

|

of two sets of random variables  and

and  for which

for which  and

and  are canonical random variables (see Canonical correlation). The problem of determining the maximum correlation coefficient between

are canonical random variables (see Canonical correlation). The problem of determining the maximum correlation coefficient between  and

and  under the conditions

under the conditions  and

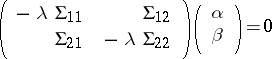

and  can be solved using Lagrange multipliers. The canonical correlation coefficients are the roots

can be solved using Lagrange multipliers. The canonical correlation coefficients are the roots  of the equation

of the equation

|

where  and

and  are the covariance matrices of

are the covariance matrices of  and

and  , respectively, and

, respectively, and  is the covariance matrix between the variables of the first and second sets. The

is the covariance matrix between the variables of the first and second sets. The  -th root of the equation is called the

-th root of the equation is called the  -th canonical correlation coefficient between

-th canonical correlation coefficient between  and

and  . It is equal to the maximum value of the correlation coefficients between the pair of linear functions

. It is equal to the maximum value of the correlation coefficients between the pair of linear functions  and

and  of canonical random variables, each of which has variance one and is uncorrelated with the first

of canonical random variables, each of which has variance one and is uncorrelated with the first  pairs of variables

pairs of variables  and

and  . The coefficients

. The coefficients  ,

,  of

of  and

and  satisfy the equation

satisfy the equation

|

when  .

.

Comments

See also Correlation; Correlation coefficient.

Canonical correlation coefficients. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Canonical_correlation_coefficients&oldid=46194