Copula

A function that links a multi-dimensional probability distribution function to its one-dimensional margins. Such functions first made their appearance in the work of M. Fréchet, W. Höffding, R. Féron, and G. Dall'Aglio. However, their explicit definition and the recognition that they are important in their own right is due to A. Sklar. Presently (1996), the best sources for information are [a1] and [a2].

A (two-dimensional) copula is a function  from the unit square

from the unit square  onto the unit interval

onto the unit interval  such that:

such that:

1)  and

and  for any

for any  ;

;

2)  whenever

whenever  and

and  .

.

If  is a copula, then

is a copula, then  is non-decreasing in each place and continuous, and hence a continuous bivariate distribution function on the unit square, with uniform margins. Furthermore, setting

is non-decreasing in each place and continuous, and hence a continuous bivariate distribution function on the unit square, with uniform margins. Furthermore, setting  , one has

, one has  for all

for all  in

in  . The functions

. The functions  and

and  are copulas, as is the function

are copulas, as is the function  given by

given by  .

.

The central Sklar theorem states that if  is a two-dimensional distribution function with one-dimensional marginal distribution functions

is a two-dimensional distribution function with one-dimensional marginal distribution functions  and

and  , then there exists a copula

, then there exists a copula  such that for all

such that for all  ,

,

|

If  and

and  are continuous, then

are continuous, then  is unique; otherwise

is unique; otherwise  is uniquely determined on

is uniquely determined on  . It follows that if

. It follows that if  and

and  are real random variables (cf. Random variable) with distribution functions

are real random variables (cf. Random variable) with distribution functions  and

and  and joint distribution function

and joint distribution function  , then there is a copula

, then there is a copula  such that

such that  . The random variables

. The random variables  ,

,  are independent if and only if it is possible to take

are independent if and only if it is possible to take  .

.

Sklar's theorem shows that much of the study of joint distribution functions can be reduced to the study of copulas. Furthermore, under a.s. strictly increasing transformations of  and

and  , the copula

, the copula  is invariant, while the margins may be changed at will. Thus (for random variables with continuous distribution functions) the study of rank statistics (insofar as it is the study of properties invariant under increasing transformations, cf. Rank statistic) may be characterized as the study of copulas and copula-invariant properties.

is invariant, while the margins may be changed at will. Thus (for random variables with continuous distribution functions) the study of rank statistics (insofar as it is the study of properties invariant under increasing transformations, cf. Rank statistic) may be characterized as the study of copulas and copula-invariant properties.

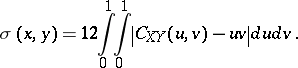

For random variables with continuous distribution functions, the extreme copulas  and

and  are attained precisely when

are attained precisely when  is a.s. an increasing (respectively, decreasing) function of

is a.s. an increasing (respectively, decreasing) function of  . Hence, copulas can be used to construct non-parametric measures of dependence. One such is the quantity

. Hence, copulas can be used to construct non-parametric measures of dependence. One such is the quantity

|

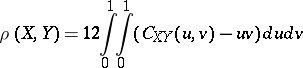

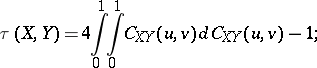

Furthermore, in terms of copulas, the two best known non-parametric measures of dependence, namely Spearman's measure of dependence  and Kendall's measure of dependence

and Kendall's measure of dependence  , are given by

, are given by

|

and

|

and the fact that  and

and  are positively quadrant dependent is succinctly expressed by the condition

are positively quadrant dependent is succinctly expressed by the condition  .

.

Several classes of copulas merit special attention. First, there are the Archimedean copulas, which admit the representation  with

with  a continuous decreasing convex function from

a continuous decreasing convex function from  into

into  satisfying

satisfying  . These may be used to generate various (generally, one- or two-parameter) families of bivariate distribution functions, and, as a consequence, play an important role in modelling non-normal dependence and testing for such dependence [a4].

. These may be used to generate various (generally, one- or two-parameter) families of bivariate distribution functions, and, as a consequence, play an important role in modelling non-normal dependence and testing for such dependence [a4].

Next, there are the shuffles of  . These are obtained by redistributing the mass distribution of

. These are obtained by redistributing the mass distribution of  (which is uniformly distributed on the main diagonal of the unit square) in such a way that the resultant mass distribution remains singular. These shuffles are dense in the space of all copulas. Nevertheless, it is still true that if

(which is uniformly distributed on the main diagonal of the unit square) in such a way that the resultant mass distribution remains singular. These shuffles are dense in the space of all copulas. Nevertheless, it is still true that if  and

and  are random variables whose copula is a shuffle of

are random variables whose copula is a shuffle of  , then there is an invertible function

, then there is an invertible function  such that

such that  . This yields the striking fact that for any pair of independent random variables

. This yields the striking fact that for any pair of independent random variables  there is a pair of random variables

there is a pair of random variables  having the same individual distribution functions as

having the same individual distribution functions as  and having a copula arbitrarily close to

and having a copula arbitrarily close to  , but such that each is completely determined by the other. (See the Mikusińksi–Sherwood–Taylor paper in [a1].)

, but such that each is completely determined by the other. (See the Mikusińksi–Sherwood–Taylor paper in [a1].)

Lastly, a copula determines a doubly-stochastic measure on the unit square. Such measures have been of interest for a long time and considerable effort has been devoted to finding extreme points of this convex set. Here, an approach using copulas has led to several new classes of such extreme points, the hairpins and generalized hairpins, as well as to further insight into the general problem. (See the Mikusińksi–Sherwood–Taylor paper in [a1].)

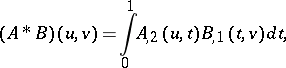

Let  be the binary operation defined on the set of two-dimensional copulas by

be the binary operation defined on the set of two-dimensional copulas by

|

where  denotes the partial derivative of

denotes the partial derivative of  with respect to its second argument and

with respect to its second argument and  the partial derivative of

the partial derivative of  with respect to its first argument (these partial derivatives exists almost everywhere). Then

with respect to its first argument (these partial derivatives exists almost everywhere). Then  is a copula, and the set of copulas is a semi-group under the operation

is a copula, and the set of copulas is a semi-group under the operation  . The salient fact concerning this operation is the following: If

. The salient fact concerning this operation is the following: If  is a real stochastic process with parameter set

is a real stochastic process with parameter set  and if

and if  is the copula of

is the copula of  and

and  , then the transition probabilities of the process satisfy the Kolmogorov–Chapman equation if and only if

, then the transition probabilities of the process satisfy the Kolmogorov–Chapman equation if and only if  for all

for all  such that

such that  . This result is the key to a new approach to the theory of Markov processes (cf. Markov process) and to a new way of constructing them. It also leads to an interesting area of functional analysis: the study of Markov algebras, [a3].

. This result is the key to a new approach to the theory of Markov processes (cf. Markov process) and to a new way of constructing them. It also leads to an interesting area of functional analysis: the study of Markov algebras, [a3].

Finally, the concept of a copula can be extended to  dimensions. An

dimensions. An  -copula may be viewed as an

-copula may be viewed as an  -dimensional distribution function whose support is in the unit

-dimensional distribution function whose support is in the unit  -cube and whose one-dimensional margins are uniform. If

-cube and whose one-dimensional margins are uniform. If  is an

is an  -dimensional distribution function with one-dimensional margins

-dimensional distribution function with one-dimensional margins  , then there is an

, then there is an  -copula

-copula  such that

such that

|

for all  . Moreover, for any

. Moreover, for any  -copula:

-copula:

|

|

however, while the upper function is an  -copula for any

-copula for any  , the lower function is not an

, the lower function is not an  -copula for any

-copula for any  .

.

A basic problem in the theory of copulas is that of compatibility, i.e., to determine which sets of copulas (of possible different dimensions) can appear as margins of a single higher-dimensional copula.

References

| [a1] | "Advances in probability distributions with given marginals: beyond the copulas" G. Dall'Aglio (ed.) S. Kotz (ed.) G. Salinetti (ed.) , Kluwer Acad. Publ. (1991) |

| [a2] | "Distributions with fixed marginals and related topics" L. Rüschendorf (ed.) B. Schweizer (ed.) M.D. Taylor (ed.) , Lecture Notes Monograph Ser. , 28 , Inst. Math. Stat. (1996) |

| [a3] | W.F. Darsow, B. Nguyen, E.T. Olsen, "Copulas and Markov processes" Ill. J. Math. , 36 (1992) pp. 600–642 |

| [a4] | C. Genest, L.-P. Rivest, "Statistical inference procedures for bivariate Archimedean copulas" J. Amer. Statist. Assoc. , 88 (1993) pp. 1034–1043 |

Copula. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Copula&oldid=19072