Empirical distribution

sample distribution

A probability distribution determined from a sample for the estimation of a true distribution. Suppose that results  of observations are independent identically-distributed random variables with distribution function

of observations are independent identically-distributed random variables with distribution function  and let

and let  be the corresponding order statistics. The empirical distribution corresponding to

be the corresponding order statistics. The empirical distribution corresponding to  is defined as the discrete distribution that assigns to every value

is defined as the discrete distribution that assigns to every value  the probability

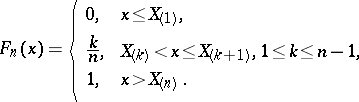

the probability  . The empirical distribution function

. The empirical distribution function  is the step-function with steps of multiples of

is the step-function with steps of multiples of  at the points defined by

at the points defined by  :

:

|

For fixed values of  the function

the function  has all the properties of an ordinary distribution function. For every fixed real

has all the properties of an ordinary distribution function. For every fixed real  the function

the function  is a random variable as a function of

is a random variable as a function of  . Thus, the empirical distribution corresponding to a sample

. Thus, the empirical distribution corresponding to a sample  is given by the family of random variables

is given by the family of random variables  depending on the real parameter

depending on the real parameter  . Here for a fixed

. Here for a fixed  ,

,

|

and

|

In accordance with the law of large numbers,  with probability one as

with probability one as  for every

for every  . This means that

. This means that  is an unbiased and consistent estimator of the distribution function

is an unbiased and consistent estimator of the distribution function  . The empirical distribution function converges, uniformly in

. The empirical distribution function converges, uniformly in  , with probability 1 to

, with probability 1 to  as

as  , i.e., if

, i.e., if

|

then

|

(the Glivenko–Cantelli theorem).

The quantity  is a measure of the proximity of

is a measure of the proximity of  to

to  . A.N. Kolmogorov found (in 1933) its limit distribution: For a continuous function

. A.N. Kolmogorov found (in 1933) its limit distribution: For a continuous function  ,

,

|

If  is not known, then to verify the hypothesis that it is a given continuous function

is not known, then to verify the hypothesis that it is a given continuous function  one uses tests based on statistics of type

one uses tests based on statistics of type  (see Kolmogorov test; Kolmogorov–Smirnov test; Non-parametric methods in statistics).

(see Kolmogorov test; Kolmogorov–Smirnov test; Non-parametric methods in statistics).

Moments and any other characteristics of an empirical distribution are called sample or empirical; for example,  is the sample mean,

is the sample mean,  is the sample variance, and

is the sample variance, and  is the sample moment of order

is the sample moment of order  .

.

Sample characteristics serve as statistical estimators of the corresponding characteristics of the original distribution.

References

| [1] | L.N. Bol'shev, N.V. Smirnov, "Tables of mathematical statistics" , Libr. math. tables , 46 , Nauka (1983) (In Russian) (Processed by L.S. Bark and E.S. Kedrova) |

| [2] | B.L. van der Waerden, "Mathematische Statistik" , Springer (1957) |

| [3] | A.A. Borovkov, "Mathematical statistics" , Moscow (1984) (In Russian) |

Comments

The use of the empirical distribution in statistics and the associated theory has been greatly developed in recent years. This has been surveyed in [a2]. For the developments in strong convergence theory associated with the empirical distribution see [a1].

References

| [a1] | M. Csörgö, P. Révész, "Strong approximation in probability and statistics" , Acad. Press (1981) |

| [a2] | G.R. Shorack, J.A. Wellner, "Empirical processes with applications to statistics" , Wiley (1986) |

| [a3] | M. Loève, "Probability theory" , Princeton Univ. Press (1963) pp. Sect. 16.3 |

| [a4] | P. Gaenssler, W. Stute, "Empirical processes: a survey of results for independent and identically distributed random variables" Ann. Prob. , 7 (1977) pp. 193–243 |

Empirical distribution. Encyclopedia of Mathematics. URL: http://encyclopediaofmath.org/index.php?title=Empirical_distribution&oldid=11280